FIRE isn’t one-size-fits-all. Choose the one that fits your goals

Not every Indian wants to retire early but everyone wants freedom. Here's how to find your path.

At 25, you’re told two things:

“Start investing early”

“Retire by 40 and chill”

But what does that even look like?

The internet throws around words like FIRE Financial Independence, Retire Early but there’s not one FIRE. There are three distinct paths that fit different lifestyles.

This post will explain:

What Lean FIRE, Coast FIRE, and Barista FIRE mean

Why they matter in the Indian context

How to decide which one suits your mindset, lifestyle, and career goals

The step-by-step plan and frameworks to follow

How to factor in personal inflation

Because at 25, you don’t need to chase a dream.

You need to design one that matches your version of enough.

First, what is FIRE?

FIRE = Financial Independence, Retire Early

At its core, it means building enough assets that you no longer have to work for money.

But how much you need and how you get there varies.

That’s where Lean, Coast, and Barista come in.

Lean FIRE : Freedom through frugality

What it means:

You accumulate enough money to retire early, living on a minimal lifestyle low expenses, simple living, no frills.

Key traits:

Annual spending: ₹10–12L (or less)

Investment corpus needed: ~₹4–5 crore

Heavy saving early, extreme discipline

Not for luxury seekers

Why it appeals:

If you value time over things, don’t mind small cities or minimalist living, Lean FIRE gives you full control.

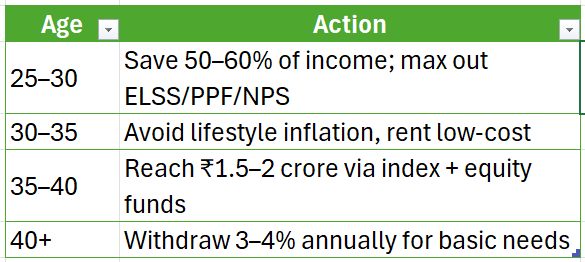

How to reach lean FIRE (step-by-step):

Tip:

Use low-cost index funds and tax-advantaged instruments (like PPF) to stretch the corpus.

Coast FIRE : Save aggressively, then let it ride

What it means:

You save aggressively in your 20s, then stop new investments by 35 and let compounding take over. You continue working, but only for expenses not retirement.

Key traits:

Corpus target: ₹2–3 Cr by age 35

Full retirement corpus builds on autopilot by 60

You can coast through low-stress jobs after 35

No pressure to save more just don’t withdraw

Why it appeals:

Perfect for someone who wants to take risks, change careers, or downshift in their 30s, without giving up the FIRE dream.

How to reach coast FIRE (step-by-step):

Tip: Combine this with freelancing or a creative career post-35.

Barista FIRE : Half retirement + Part-time income

What it means:

You semi-retire early, with a corpus that covers some expenses. The rest comes from a low-stress part-time job or side hustle.

Key traits:

Corpus: ₹1–2 crore

Part-time income: ₹60K–80K/month

Lifestyle: Balanced travel, hobbies, flexibility

Good for those who don’t want full retirement, but want freedom

Why it appeals:

For Indians who like to work but not under pressure. Ideal if you want to freelance, teach, consult, or move to a Tier-2 city.

How to reach Barista FIRE (step-by-step):

Tip: Use hybrid equity-debt funds + invest in skill-based courses.

Which FIRE path is for you?

FIRE corpus calculation (Indian edition)

How to adjust for personal inflation

Indian inflation is personalized:

Tier-1 city rent grows at 10–12%

Children’s education inflates at 12–14%

Healthcare and lifestyle costs rise differently

Adjustment rule of thumb:

If you live in Tier 1: assume 12–14% inflation

If you plan to relocate or downsize: assume 7–8% inflation

Build FIRE plans using real returns = (Expected return - inflation)

For example:

12% equity return - 7% inflation = 5% real return

Use that to stress-test your FIRE corpus. If your inflation is even higher , then rather than increasing return , we have to start focusing on optimizing our income and expenses.

Final word: Don’t just dream of freedom, define what you’ll do with it

FIRE isn’t about escaping work.

It’s about designing life on your terms.

Some want to quit.

Some want to coast.

Some want to consult from a café.

None are wrong as long as the plan fits the person.

Pick your FIRE.

Run your numbers.

Build your buffers.

And let your future self thank you for the clarity you gave at 25.